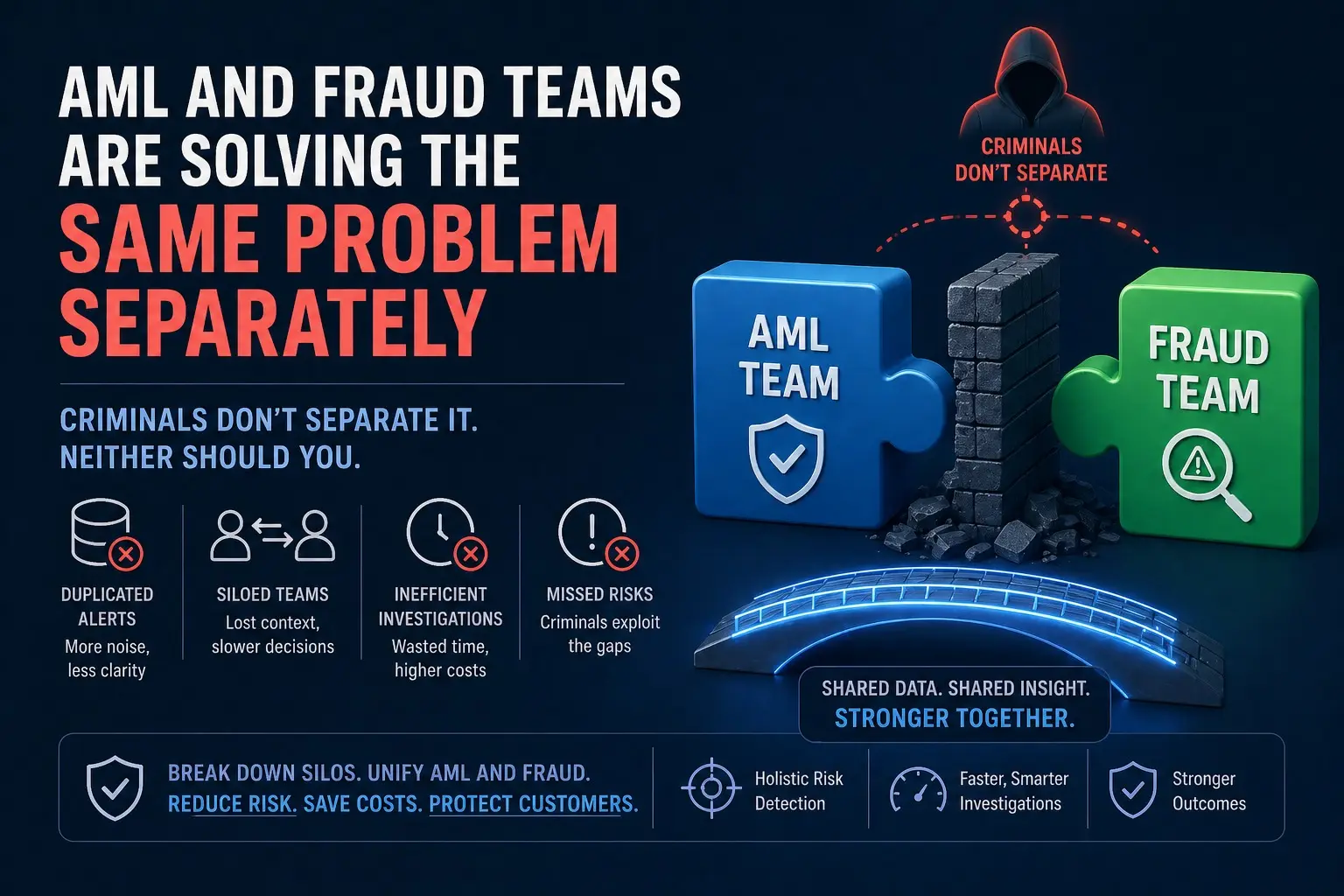

Walk into the compliance department of most financial institutions and you will find two distinct teams working in adjacent spaces with minimal overlap. The fraud team monitors real-time transaction anomalies, investigates account takeovers, and responds to disputed payments. The AML team reviews suspicious activity reports, manages watchlist screening, and files regulatory documentation.

Both teams are trying to stop financial crime. Both are doing their jobs. And in many institutions, both are operating on separate platforms, reviewing separate alert queues, and making decisions without visibility into what the other team is seeing.

This separation made sense twenty years ago when fraud was largely opportunistic, AML was primarily about large institutional players, and the overlap between the two was limited. Today that logic has collapsed. The criminal networks running authorized push payment scams are often the same ones moving proceeds through layered financial structures to obscure their origin. The account that gets taken over in a fraud scheme frequently becomes the conduit for money laundering activity two transactions later.

When fraud and AML operate in silos, financial institutions are investigating fragments of the same criminal activity in isolation. Neither team has the full picture. Neither can see the connection. And the criminal operation continues because the detection architecture was designed for a problem that no longer looks the way it used to.

How Fraud and Money Laundering Became One Problem

The clearest illustration of how fraud and AML have converged is the mule account ecosystem.

Money mule networks, where recruited individuals allow their accounts to be used to receive and forward illicit funds, sit directly at the intersection of fraud and money laundering. The account opening is often facilitated through identity fraud or document forgery, which is a fraud typology. The movement of funds through the account is layering activity, which is an AML typology. The person who recruited the mule may be operating a criminal enterprise that falls under organized crime AML frameworks.

A fraud team that detects unusual account behavior but has no visibility into the customer’s AML risk profile will investigate a transaction anomaly. An AML team reviewing the same customer’s risk profile without real-time transaction data will see a pattern, but only after the money has moved. Neither team alone can stop the operation. Together, working from a shared data environment, they have a realistic chance.

The same dynamic plays out across investment fraud, romance scams, and business email compromise. In each typology, the initial fraud enables a subsequent laundering stage. The criminal relies on the organizational and technical gap between fraud detection and AML monitoring to ensure that neither function sees the full scope of what is happening.

Institutions moving toward AI-native financial crime compliance have a structural advantage here. When transaction monitoring, watchlist screening, fraud signals, and customer risk scoring share the same data layer, the cross-functional patterns that siloed systems cannot assemble become visible. That visibility is not just operationally useful. It is increasingly what regulators expect to see when they examine how an institution identifies and escalates complex financial crime.

What Separate Infrastructure Actually Costs

The operational cost of running fraud and AML as separate functions is visible in three places.

Duplicate investigation effort. When a customer triggers alerts in both the fraud system and the AML system, analysts in each team investigate the same customer independently. They pull the same account history, review the same transaction records, and often reach similar conclusions through parallel workflows that could have been one investigation. At institutions processing large volumes, this duplication represents significant analyst time spent on redundant work.

Missed cross-signal intelligence. A fraud alert at a threshold slightly below escalation and an AML alert at a threshold slightly below escalation, occurring for the same customer within the same week, are individually unremarkable. Together, they are a pattern worth investigating urgently. Systems that do not share a common data layer cannot combine these signals. Both alerts get cleared independently. The customer remains active.

Slower response to emerging typologies. When a new fraud typology emerges that has AML implications, institutions with separate systems need to coordinate across teams to understand the full picture, update rules in two separate platforms, and train analysts in two departments. Institutions with unified infrastructure can respond with a single rule update and a shared investigation workflow. In a threat environment where new typologies can spread across the industry in weeks, response speed matters enormously.

Why the Convergence Argument Is Winning Internally

For years, the standard counter-argument against converging fraud and AML functions was regulatory. AML compliance sits under specific legislative frameworks, BSA in the US, MLRs in the UK, AMLD in the EU, with defined reporting obligations and governance structures. Fraud prevention is a different function with different metrics and often different regulatory oversight. Combining them creates complexity.

That argument has not disappeared, but it has weakened significantly as the practical costs of separation have become more visible and as regulators themselves have increasingly used language about “financial crime” as a unified concept rather than treating fraud and money laundering as entirely distinct concerns.

The UK’s Financial Conduct Authority has been notably explicit about this. Its guidance on APP fraud and its AML supervisory work are increasingly coordinated because the FCA recognizes that the criminal networks driving both operate in an integrated way. The regulatory direction of travel is toward unified financial crime risk management, not toward more rigid separation.

For a detailed breakdown of what the components of a robust, unified financial crime infrastructure look like in practice, Flagright’s framework for AML compliance and fraud prevention covers the full architecture, including how real-time transaction monitoring, customer risk assessment, KYC/KYB orchestration, and sanctions screening function as integrated components rather than standalone tools.

The Technology Gap Between Aspiration and Reality

Most financial institutions acknowledge the convergence argument intellectually. The practical barrier is infrastructure. Fraud and AML teams have often been on different platforms for years, sometimes decades. The fraud team’s real-time alerting system is deeply integrated with the payment operations workflow. The AML team’s monitoring platform is tied to regulatory reporting systems and case management workflows. Converging them is not a configuration change. It is a significant technical project.

This is where many institutions get stuck. The aspiration to unify is genuine, but the migration path looks difficult, and the risk of disrupting two live compliance functions simultaneously is real.

The answer is not a single massive migration. It is architectural alignment, moving toward a shared data layer and shared case management infrastructure that allows fraud and AML workflows to remain operationally distinct while sharing customer risk data, transaction history, and alert context. The fraud team still runs its alerts. The AML team still manages its investigation workflows. But when an analyst in either team opens a customer record, they see the full picture: every alert from every function, every investigation note, every risk signal from every source.

This is where AI Forensics changes the investigation dynamic meaningfully. Rather than each team manually reconstructing a customer’s activity history from separate systems, AI-assisted investigation surfaces the relevant context automatically, connecting behavioral patterns across fraud and AML signals in a single workflow. Critically, this works with full transparency. Analysts see the reasoning behind what the system surfaces, not just a score. They evaluate, decide, and document. Human judgment stays in control. The audit trail supports every step.

This is architecturally achievable with modern compliance platforms. The question is whether the institution has made the decision to invest in it.

Three Signals Your Fraud and AML Infrastructure Needs to Converge

Not every institution is at the same point in this journey. These are the operational signals that suggest the separation has become a problem worth solving now rather than later.

You Are Investigating the Same Customers Twice

If compliance team leads in fraud and AML can identify customers who have open investigations in both functions simultaneously with no shared case record, the duplication is already costing you analyst capacity. This is the most visible symptom of siloed infrastructure, and it is also the easiest to quantify for a business case.

Your Rule Coverage Has Gaps at the Boundary

Fraud rules are typically optimized for speed, catching anomalies in real time. AML rules are typically optimized for pattern detection across longer time horizons. There is a class of activity that falls between these optimization targets: behavioral patterns that develop over days rather than seconds but are not yet reportable as suspicious under AML thresholds. These patterns are most visible when fraud and AML monitoring share a timeline view of the same customer. In siloed systems, they fall through.

Your Regulatory Reporting Is Retrospective, Not Anticipatory

When SAR filings consistently describe activity that the institution detected, investigated, and reported after the fact, rather than activity that was caught in near-real-time and stopped, it is a signal that the detection infrastructure is not fast enough or integrated enough to enable proactive intervention. The filing obligation is being met. The prevention obligation is not.

What Good Financial Crime Infrastructure Looks Like

The institutions that have made meaningful progress on unifying fraud and AML share some common architectural choices.

A single customer risk profile that aggregates signals from onboarding, screening, transaction monitoring, fraud detection, and case management into one dynamic record. Every function that touches the customer updates the same profile. Every analyst who opens the customer record sees the same information.

Shared case management that does not force analysts to work in separate systems for fraud and AML cases. When a case involves both typologies, it stays in one place with a unified investigation record.

Configurable rule logic that compliance teams can adjust without engineering involvement. Financial crime typologies do not wait for quarterly release cycles. The teams that can reconfigure detection rules quickly respond to new threats quickly. Those that cannot remain on a lag.

AI-assisted triage that explains itself. This point is critical. AI that surfaces recommendations with visible reasoning allows analysts to evaluate suggestions rather than accept scores. It also allows institutions to defend their detection decisions to regulators with a clear audit trail, not just a model output.

Real-time monitoring across both functions. Real-time fraud detection and batch AML monitoring running on the same customer creates a detection asymmetry that criminals can exploit. Both functions need to operate at the speed that the threat requires.

Flagright is trusted by more than 100 financial institutions across 30-plus countries precisely because its platform was built around this unified model from the ground up. Transaction monitoring, watchlist screening, investigations, and governance share a single audit-ready system rather than being connected through fragile integrations. For institutions that have outgrown the siloed architecture their compliance programs started with, that foundation matters more than any individual feature the platform offers.

The institutions building toward this model are not doing so because convergence is theoretically elegant. They are doing so because the alternative, running separate functions on separate platforms with separate data, has a documented operational cost in missed detections, duplicated effort, and regulatory exposure.

Financial crime does not organize itself around the org chart of the institutions it targets. The compliance infrastructure that catches it needs to be at least as integrated as the threats it is designed to stop.

Also Read